Struggling To Save 💵 Money? Avoid These Common Financial Mistakes!

As we progress in life, it is safe to say an individual is much more stable and focused in the 30s compared to the 20s (most of the time). You are mostly sorted out with the life partner and the struggles of 20s would have given life lessons & experiences that one would want to capitalize and built upon for times to come.

Although the money traps being discussed in this writeup are targeted to the age group of 30s, but in general the same can be applied to anyone seeking to improve their finances. Before we go deep into the 5 points, I would highly recommend you to make sure you have your emergency fund set up which should at least be 3-6 months of monthly expense saved into your bank account OR invested in a place where you can liquidate within a few days notice. I have discussed emergency fund allocation in detail in an old video here and working on an updated version too.

There as an article by Bloomberg on how 1/3rd of the people in the USA earning more than $250k a year still live pay check to pay check. I wrote a twitter thread on this as well stressing on the fact that financial freedom target do not realize simply with earning more, but it comes with a combination of income and money management – it has to be noted that making money is very important, but retaining and growing what you earned is more important and matters the most!

Lets talk about those 5 money traps one by one below 🔽

1 – EXPENSIVE HOUSE 🏡!

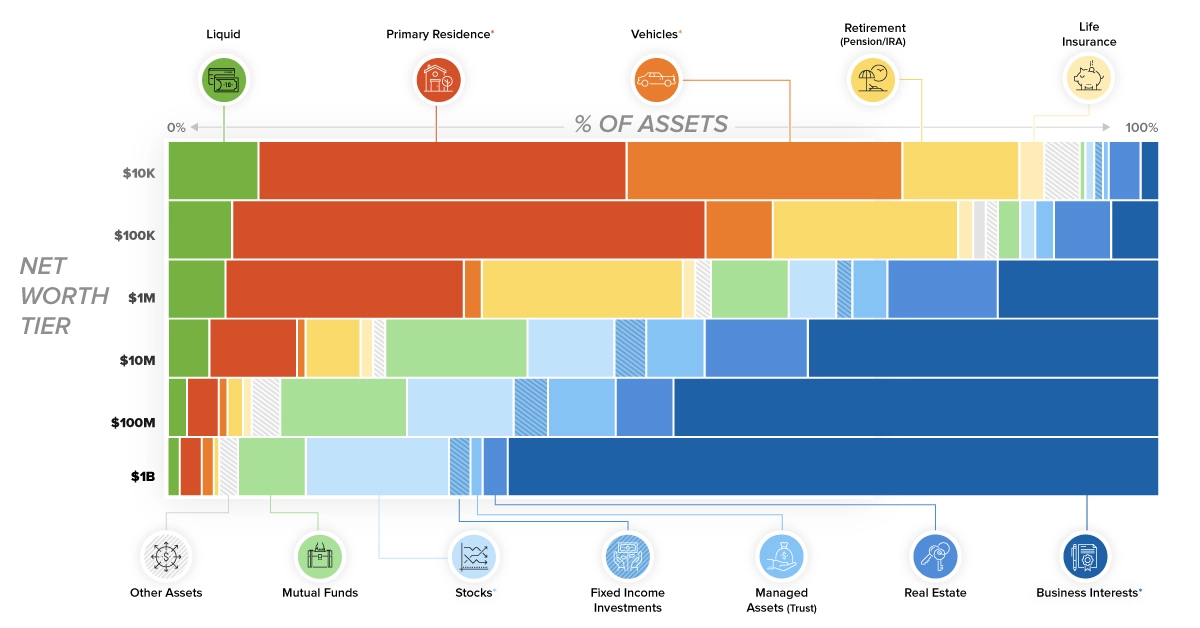

In a south asian household – one thing always on top of someone’s mind is their “own home” – and it carries significant prestige in the society. House carries a significant chunk of middle-class house hold’s networth which I already have discussed in this video here and a great infographic from visual capitalist can be seen as well below – however, before making such an investment a lot of working should be performed.

One has to analyze all associated expenses after the home ownership becomes reality like taxes, interest payments (in case the house is mortgaged), furniture, renovation cost and a host of other expenses which comes as part and parcel of becoming a landlord.

I am assuming here that the house is being purchased through mortgage, so based on the above – one should always keep headroom for monthly installments as after becoming the landlord you will get bills like property tax, major maintenance bills, service charges, variable interest payments on top of principal payment, insurance cost in some cases & above all working out solution for that house at the time of relocation to other city/country due to one’s work location.

For Pakistan, there has been an incentive by the government for subsidized loan program called as "Mera Pakistan Mera Ghar" which provides loan for upto 10Million PKR and should be considered by everyone to realize owning the home.

However, with any mortgage, never consider taking a loan to pay for the down payment – in case you you dont have the funds to pay for the upfront cost of financing the house, save up and only then think about it.

Having said all this, a house is still a very good investment if all above considerations are kept in mind and the decision to buy a particular house is taken above any bias from the society or peer pressure.

2 – FANCY CAR 🚘!

A new car outside your house looks very nice and it fulfills your desire to show to the world about your “achievement” as well. However, this wont go well with your finances in case the car is bank financed while you struggle to pay the monthly installments, fuel and insurance.

Like you house, your car also need cost to keep it running. I have discussed in a video uploaded before how people in a country like Pakistan cannot afford to pay the electricity bills and will stop using air conditioners but prefer to have a new car outside their homes! We have observed such scenarios in our daily lives and a video uploaded before talks about such life style inflation issues in the society.

3 – BUYING WRONG INSURANCE 📑 (or not buying at all)

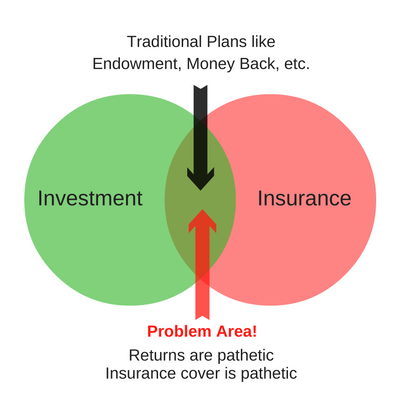

This is a very important point which need to be read by everyone regardless of their age. We have seen the scams where people loose their savings under the guise of high returns and insurance cover!

First of all, understand what you are investing or buying into. As a rule of thumb, just don’t try to combine insurance with investment – as a result you will know where your money is going to and you don’t have to justify the insurance with investment and vice versa. Make sure to keep these two segregated in order to avoid biases. There has been a twitter awareness drive as well and you can follow those accounts to make sure you don’t buy an insurance that you dont understand well.

Insurance is a sunk cost – but it will come to help you at the time when you really need it – take an example of car insurance which is still not mandatory in a country like Pakistan, however, it is recommended to an extent that you should factor in the cost of insurance before buying the car and if you cannot make room for insurance in the budget, then you must reduce the cost of car to accommodate the insurance cost.

Similarly, as I discussed in this video a few points regarding the expats in the gulf where one of the key factor is to make sure to buy health insurance for self and family if not provided by the company. This applies to everyone specially someone in the age of 30s as here one is raising young family and at the same time have aging parents, so it makes perfect sense to have an umbrella of good health insurance all the time.

4 – MINIMUM PAYMENT FOR CREDIT CARDS 💳!

There should be a proper test before someone is eligible for having a credit card – just like a driving license test. A car can bring so much of value to ones life, similarly credit cards also have a huge potential which can open a whole lot of opportunities in personal finance space. However, the problem is that the credit cards are not used properly by the masses and hence have a bad name across the communities. I have discussed the best possible way credit cards can be used in this video and possible areas where credit cards should be avoided completely in this video.

One of the main misconceptions of using credit card is to carry on the debt and keep paying the minimum payments which is a recipe of long term disaster. As mentioned before, one should have a proper training to use credit card and staying away from minimum payment regime should the compulsory in that training.

Just to explain – if someone decides to pay only the minimum payment on credit card with PKR 8000 of debt without spending anything in future on the same card, it will take 23 years to just completely payoff the debt while still paying roughly 11,000 PKR in interest.

5 – INVESTING TOO CONSERVATIVELY 📉!

When you are young, specially in the 30s while being stable in career and with stable income, you should not stay back from investing aggressivly. However, one should keep diversified in assets which have proven track record of growing the wealth over long period of time as time is still on your side.

People tend to invest with caution or invest in instruments which are made for retirees like fixed deposits because of the assumed safety net – in your 30s, one should have minimum investment towards components in conservative assets (like fixed deposits) and have high stakes in aggressive assets (like stocks) with a long term vision.

This however does not mean that you should invest in all kind of ponzi schemes with glitz and glamor without due diligence as in today’s world it’s very easy to get influenced and loose all your hard earned funds in such schemes – You must read this writeup about fixed income and what is the catch with it for better understanding. I have learnt this the hard way – Here is a video of mine explaining my way to grow the assets from my early 20s till now.

About Myself

I post 3 videos every week on my YouTube channel on the topics of productivity & personal finance specifically for expats & in general for wider Pakistani community. Besides this, I update this website / blog on weekly basis so do visit regularly for updates – To get value out of the content, please consider subscribing both the YouTube channel and the newsletter.

Videos uploaded in last few days, in case you missed

My social media handles:

Twitter

Instagram

Facebook

Linkedin

Tiktok

Youtube (Main channel)

YouTube (Q&A Clips channel)

KEEP HUSTLING 😉